Why XRP Price Has Failed To Capture XRPL’s Growing Adoption in 2026

Key Insights:

- XRPL is becoming TradFi-friendly rails for tokenized funds and stablecoins but the high adoption rate is yet to drive XRP price action.

- XRPL adoption doesn’t guarantee XRP demand because stablecoins can do most settlement.

- Fees and reserves create a small baseline but don’t scale with dollar value moved.

- XRP wins if it becomes the liquidity bridge that market makers must hold.

- ETFs/treasuries can tighten supply fastest by locking up XRP off-ledger.

XRP price action has yet to reflect the growing adoption of the XRP Ledger, which is increasingly resembling financial plumbing that traditional institutions can plug into without rebuilding their entire systems.

Tokenized funds can live on the ledger, and stablecoins can move across it quickly and with finality. At the same time, the network keeps adding features for regulated players who want on-chain settlement, but not an open door to every unknown counterparty.

That progress creates a positive environment for XRP holders. However, a busy XRPL has not automatically translated into booming demand for XRP.

XRPL Wins Adoption, XRP Price Fails to Capture the Upside

In 2026, the ledger can thrive as infrastructure while XRP only collects a thin slice of utility, unless the market starts treating XRP as the main liquidity unit.

The first link between usage and XRP is simple: fees. Every transaction incurs fees in XRP, and the protocol burns those fees rather than paying them out to validators. That design helps defend the network from spam, which is smart. Still, it does not create the kind of visible cash flow that investors can easily price like a business. The burn math also stays small at normal fee levels.

A million transactions at the base fee burns only about 10 XRP. And if fees ever rise enough to matter, the network is probably congested, which is the opposite of what payment rails want. So yes, XRP gets consumed, but fee burn alone rarely becomes a valuation engine.

XRP Reserves: XRP Demand for Reserves Provides A Better Metric For Capturing XRP Price Action

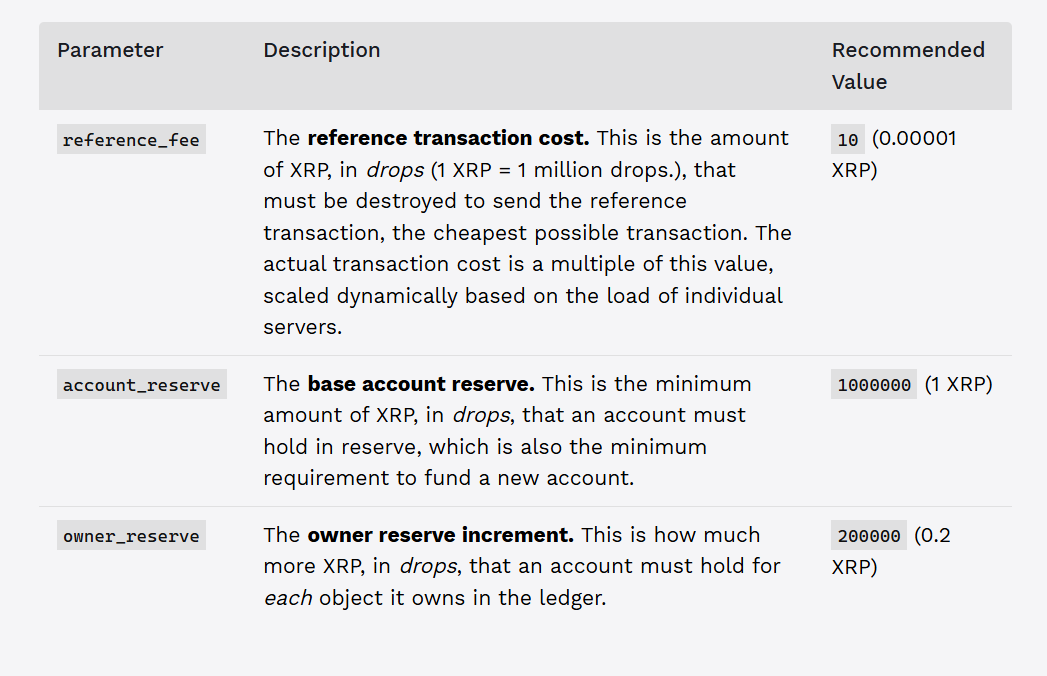

Reserves offer a more measurable source of structural demand. XRPL requires XRP reserves to open accounts and to hold certain ledger objects, such as trust lines, offers, and escrows. The current requirements sit around 1 XRP per account and 0.2 XRP per owned item, with small exceptions for brand-new accounts.

XRP price news: Validator parameters on XRPL

XRP price news: Validator parameters on XRPL

This mechanism locks XRP in place as activity grows, but it scales with the number of users and objects, not with the dollar value of what settles. A large tokenized fund can sit in a small number of issuer accounts, while a million retail users creating trust lines and offers can immobilize far more XRP in total.

Here’s the small detail that matters. In December 2024, XRPL made the network easier to use by slashing its reserve rules. The base reserve dropped from 10 XRP to 1 XRP. The owner’s reserve also fell from 2 XRP to 0.2 XRP.

With this change, Ripple lowered the barrier to entry and made the network easier to use. As such, the trade-off is easy, with smaller reserves, less XRP gets locked up. Hence, the scarcity boost from reserves is weaker.

Reserves can still matter if XRPL experiences an object explosion, where accounts and on-ledger objects multiply across millions of participants. However, reserves do not rise automatically just because tokenized asset headlines get bigger.

If fees and reserves form the floor, liquidity is where XRP can truly capture upside. XRP matters most when it becomes the bridge asset that market makers and institutions must hold as working capital to route flows and quote tight spreads.

XRP Needs To Be The Centre of XRPL Liquidity & Not Stablecoins

A simple inventory framing explains the difference. At $1 trillion in XRP-mediated payments per year, daily flow is roughly $2.74 billion. If liquidity providers hold about half a day of buffer, that implies around $1.37 billion of XRP inventory. At roughly $1.39 per XRP, that translates to about 986 million XRP held as working capital, a meaningful sink if sustained.

Yet this is also where XRPL growth can bypass XRP. If stablecoins become the main unit of account on XRPL, then stablecoin-to-stablecoin routing can expand without forcing participants to hold much XRP beyond fees and reserves. In that world, XRPL stays busy while XRP remains optional.

Another major off-ledger scarcity channel is regulated wrappers that warehouse XRP. After the SEC ended the Ripple lawsuit in August 2025, institutional access constraints eased. Since then, U.S. spot XRP ETFs have appeared, with assets reported above $1 billion.

The mechanism is straightforward. Each $1 billion of net ETF demand can lock up roughly $1 billion in custody, divided by the XRP price, which is about 719 million XRP at $1.39. Investors also understand this model quickly because it mirrors commodity ETFs that reduce free float without needing on-chain revenue.

XRPL Improvements in 2026

Meanwhile, the protocol itself keeps evolving, but institutions still choose what becomes essential. Early 2026 Ripple news releases showed both ambition and caution. Rippled v3.1.0 added Single Asset Vaults and a lending-related amendment, while v3.1.1 later disabled batch-related changes after a severe bug.

On top of that, institution-focused features like Permissioned Domains and Permissioned DEXs aim to create gated venues where only approved participants can trade. These tools can help XRPL win pilots, and production flows from firms that avoid open order books.

Still, those venues can settle stablecoin-to-stablecoin and clear tokenized funds in issued units while minimizing XRP exposure, unless liquidity conventions place XRP at the center.

The stakes are higher now because XRPL is not just trying to beat other crypto networks. It is also trying to earn a spot in the wider plumbing of global payments, alongside stablecoin networks, bank-led settlement groups, and even state-backed systems. Some industry estimates put cross-border payment flows in the hundreds of trillions of dollars, with forecasts around $290 trillion by 2030, and reports have also said China’s multi-CBDC project mBridge has already processed more than $55 billion.

So the core distinction keeps returning. XRPL can create enormous network value, but XRP price captures only through specific plumbing: fees, reserves, liquidity inventory, and regulated warehousing. For holders, the bull case is not simply more XRPL activity. The bull case is XRPL growth that forces routing, quoting, and liquidity to run through XRP.

The post Why XRP Price Has Failed To Capture XRPL’s Growing Adoption in 2026 appeared first on The Coin Republic.

You May Also Like

SEC issues advisory on unregistered ‘Salmon’ and ‘Mabilis’ lending apps

Too soon to know how Iran war will affect inflation