What’s the intention behind a radical proposal to burn 45% of HYPE’s supply?

Author: David, TechFlow

Recently, amid the Perp DEX craze, various new projects have sprung up like mushrooms after rain, constantly challenging Hyperliquid's status as the big brother.

With so much attention focused on the innovations of new players, the price fluctuations of the leading token, $HYPE, have been overlooked. However, the most direct correlation to token price fluctuations is the supply of $HYPE.

What affects the supply is, first, continuous repurchases, which is equivalent to constantly buying in the stock market to reduce circulation and reduce the water in the pool; and the other is the adjustment of the overall supply mechanism, which is equivalent to turning off the tap.

A closer look at $HYPE's current supply design reveals issues:

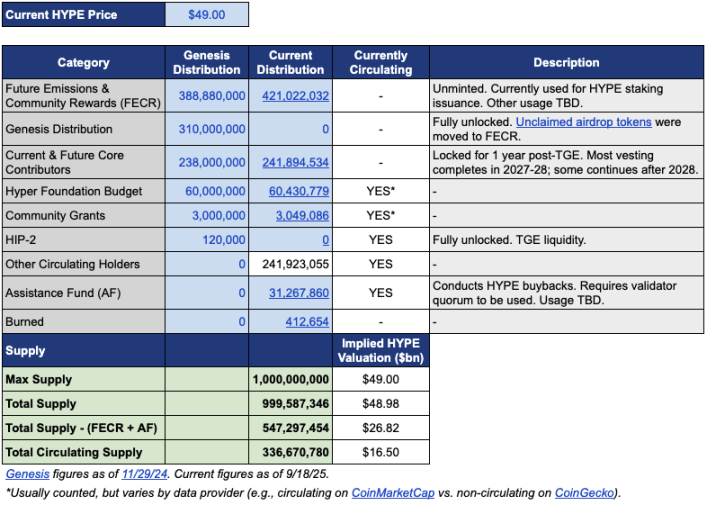

The circulating supply is approximately 339 million coins, with a market capitalization of approximately $15.4 billion; however, the total supply is close to 1 billion coins, with an FDV of up to $46 billion.

The nearly threefold gap between MC and FDV comes mainly from two parts: 421 million tokens allocated to the Future Emissions and Community Rewards (FECR) and 31.26 million tokens in the Assistance Fund (AF).

The Assistance Fund is Hyperliquid's account for repurchasing HYPE using protocol revenue. It buys HYPE daily but doesn't burn it, instead holding it. The problem is that investors often feel overvalued when they see 46 billion FDV, even though only a third of it is actually in circulation.

Against this backdrop, investment manager Jon Charbonneau (DBA Asset Management, which holds a large position in HYPE) and independent researcher Hasu released an unofficial proposal for $HYPE on September 22nd. The content is very radical; the simplified version is:

Burning 45% of the current total $HYPE supply will bring FDV closer to its actual circulation value.

This proposal quickly sparked community discussion, and as of press time, the post had received 410,000 views.

Why such a strong response? If the proposal is adopted, burning 45% of the HYPE supply means the value of each HYPE token will almost double. A lower FDV may also attract investors who were previously on the sidelines.

We have also quickly summarized the content of the original post of this proposal and organized it below.

Reduce FDV to make HYPE look less expensive

Jon and Hasu's proposal looks simple, burning 45% of the supply, but the actual operation is more complicated.

To understand this proposal, we first need to understand HYPE's current supply structure. According to the data sheet Jon provided, at $49 (the HYPE price at the time of their proposal), of the total HYPE supply of 1 billion, only 337 million were actually in circulation, corresponding to a market capitalization of $16.5 billion.

But where did the remaining 660 million go?

The two largest pieces are: 421 million are allocated to "Future Emissions and Community Rewards" (FECR), which is equivalent to a huge reserve pool, but no one knows when and how to use it; the other 31.26 million are in the hands of the Assistance Fund (AF), which buys HYPE every day but does not sell it, and just hoards it.

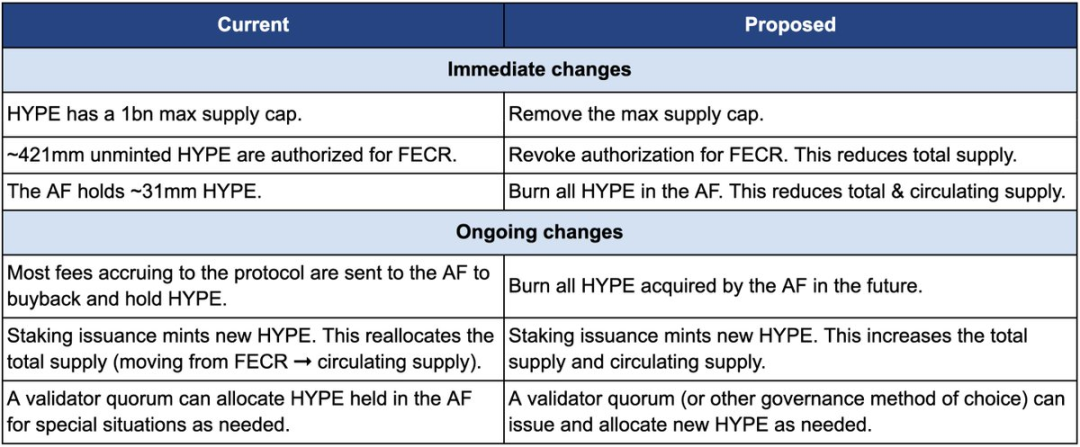

Let’s first talk about how to burn. The proposal includes three core actions:

First, the authorization for 421 million FECRs (Future Emissions and Community Rewards) was revoked. These tokens were originally intended for future staking rewards and community incentives, but there has been no clear issuance schedule. Jon believes that rather than letting these tokens hang like a sword of Damocles over the market, it would be better to directly revoke the authorization. When necessary, the issuance can be re-approved through a governance vote.

Second, the 31.26 million HYPE tokens held by the Assistance Fund (AF) will be destroyed, and all future HYPE tokens purchased by AF will also be destroyed. Currently, AF uses protocol revenue (primarily 99% of transaction fees) to repurchase HYPE daily, with an average daily purchase volume of approximately $1 million. Under Jon's plan, these purchased tokens will no longer be held but will be burned immediately.

Third, remove the 1 billion supply cap. This sounds counterintuitive: if we want to reduce the supply, why remove the cap?

Jon explained that the fixed cap is a legacy of Bitcoin's 21 million token model and is meaningless for most projects. With the cap removed, any future issuance of new coins (such as staking rewards) could be determined through governance, rather than allocated from a reserved pool.

The comparison table below clearly shows the changes before and after the proposal: the left side is the current situation, and the right side is the situation after the proposal.

Why are they so radical? The core reason given by Jon and Hasu is that HYPE’s token supply design is an accounting issue, not an economic issue.

The problem lies in the calculation methods of major data platforms such as CoinmarketCap.

Each platform handles burned tokens, FECR reserves, and AF holdings differently when calculating FDV, total supply, and circulating supply. For example, CoinMarketCap always uses a maximum supply of 1 billion to calculate FDV, and does not adjust even if tokens are burned.

The result is that no matter how HYPE repurchases or burns it, the displayed FDV cannot be reduced.

It can be seen that the biggest change in the proposal is that 421 million FECR and 31 million AF will disappear, and the 1 billion hard cap will also be cancelled and replaced by issuance through governance as needed.

Jon wrote in the proposal: "Many investors, including some of the largest and most mature funds, only look at the superficial FDV numbers." With a FDV of $46 billion, HYPE looks more expensive than Ethereum. Who would dare to buy it?

However, most proposals seem to be driven by one's own opinion. Jon explicitly stated that the DBA Fund he manages holds a "material position" in HYPE, which he personally holds as well, and that if there were a vote, they would vote in favor.

The proposal concludes by emphasizing that these changes will not affect the relative shares of existing holders, will not affect Hyperliquid's ability to fund projects, and will not change the decision-making mechanism. In Jon's words,

“It just keeps the books more honest.”

When “distribution to the community” becomes an unspoken rule

But will the community buy into this proposal? The original post's comments section has already exploded.

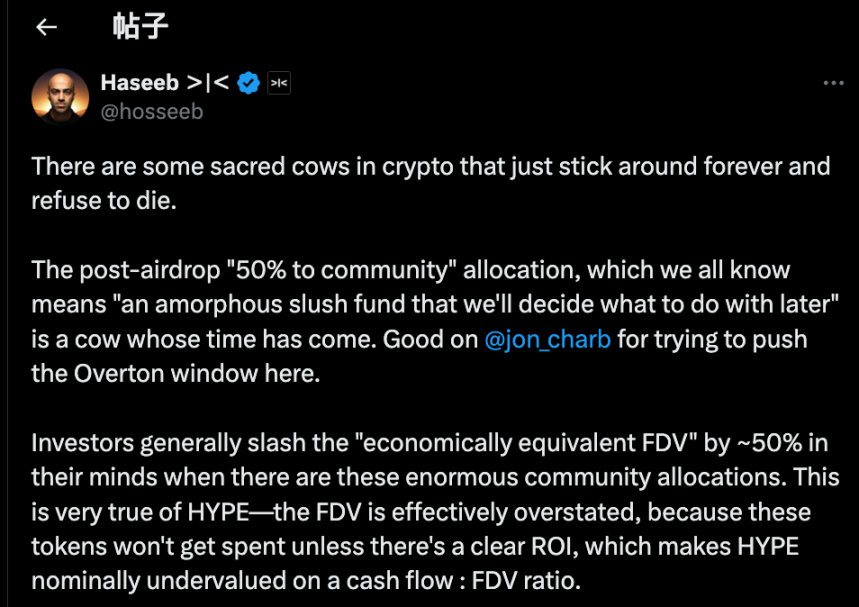

Among them, Dragonfly Capital partner Haseeb Qureshi's comments put this proposal into a larger industry context:

“Some of the ‘sacred cows’ in the crypto industry just won’t die, and it’s time to slaughter them.”

He was referring to an unspoken rule throughout the crypto industry: after tokens are generated, projects must always reserve 40-50% of their tokens for the "community." This sounds very decentralized and Web3-esque, but it's actually a form of performance art.

In 2021, at the height of the bull market, every project was competing to be more "decentralized." Consequently, token economics specifications included claims of 50%, 60%, or even 70% community ownership, with the higher the number, the more politically correct it seemed.

But how exactly will these tokens be used? No one can explain.

From a more malicious perspective, some project parties are more realistic about the tokens they allocate to the community, allowing them to use them whenever and however they want, under the euphemism of "for the community."

The problem is, the market is not stupid.

Haseeb also revealed an open secret: professional investors automatically give these "community reserves" a 50% discount when evaluating projects.

A project with a FDV of 50 billion but 50% of it allocated to the community is only worth 25 billion in their eyes. Unless there is a clear ROI, these tokens are just empty promises.

This is precisely the problem HYPE faces. Of HYPE's $49 billion in FDV, over 40% is reserved for "future emissions and community rewards." This figure can be dissuading for investors.

It's not because HYPE is bad, but because the numbers on paper are too inflated. Haseeb believes that Jon's proposal has a driving effect, gradually turning radical ideas that were originally not openly discussed into acceptable mainstream views; we need to question the crypto industry's practice of allocating tokens to "community reserves."

To summarize, the supporters' argument is simple:

If you want to use tokens, you need to implement governance, clearly stating why they are being issued, how much to issue, and what the expected returns are. It should be transparent and accountable, not a black box.

At the same time, because this post is too radical, there are some objections in the comment section. We can summarize it into three parts:

First, some HYPE must be used as a risk reserve.

From a risk management perspective, some believe the 31 million HYPE in the AF support fund isn't just inventory, but also emergency funds. What if regulatory fines or hacker attacks require compensation? Burning all the reserves would eliminate the crisis buffer.

Second, HYPE already has a complete destruction mechanism technically.

Hyperliquid already has three natural destruction mechanisms: spot transaction fee destruction, HyperEVM gas fee destruction, and token auction fee destruction.

These mechanisms automatically adjust supply based on platform usage, so why would anyone need to intervene? Usage-based destruction is healthier than a one-time destruction.

Third, large-scale destruction is not conducive to incentives.

Future emissions are Hyperliquid's most important growth tool, used to incentivize users and reward contributors. Burning them would be tantamount to self-destruction. Furthermore, large stakers would be locked out. Without new token rewards, who would be willing to stake?

Who does the token serve?

On the surface, this seems to be a technical discussion about whether to burn the coin or not. However, a closer look at the positions of all parties reveals that the disagreement is actually a matter of opinion.

The view represented by Jon and Haseeb is clear: institutional investors are the main source of incremental funds.

These funds manage billions of dollars, and their purchases can truly drive prices. The problem is, they're hesitant to enter the market when they see the $49 billion FDV. So, we need to correct this number to make HYPE more attractive to institutions.

The community's perspective is completely different. They see the platform's foundation as the retail traders who open and close positions daily. Hyperliquid's success isn't due to VC funding, but rather the support of 94,000 airdrop recipients. Changing the economic model to cater to institutions is putting the cart before the horse.

This isn't the first time this disagreement has arisen.

Looking back at DeFi history, almost every successful project has experienced a similar crossroads. When Uniswap launched its token, the community and investors argued fiercely over control of the treasury.

The core issue is always the same: Does a project on a blockchain serve big money or grassroots crypto natives?

This proposal seems to serve the former. "Many of the largest and most mature funds only look at FDV." The implication is clear: if you want to let these big money come in, you have to play by their rules.

Jon, the proposer, is an institutional investor himself, and his DBA Fund holds a significant amount of HYPE. If the proposal passes, it will be large investors like him who will benefit the most. With a reduced supply, the price of the coin is likely to rise, and the value of their holdings will also increase.

Considering Arthur Hayes' recent $800,000 sale of HYPE, which he jokingly described as buying a Ferrari, we can sense a subtle timing. The earliest backers are cashing out, and now some are proposing to burn tokens to drive up the price. Who are they actually helping?

As of press time, Hyperliquid has yet to officially release its position. Regardless of the final decision, this debate has revealed a truth that no one wants to face:

With profit at the forefront, we may never have cared that much about decentralization and were just pretending.

You May Also Like

Momentous Grayscale ETF: GDLC Fund’s Historic Conversion Set to Trade Tomorrow

The UA Sprinkler Fitters Local 669 JATC – Notice of Privacy Incident